The 2026 Tax Prep Survival Guide: 5 Steps to Avoid IRS Delays With Clean QuickBooks Online Bookkeeping

- The Team

- Feb 9

- 5 min read

Let's be honest: nobody wants to hear from the IRS in July because your tax return doesn't match what they have on file.

But here's the thing: most IRS delays and notices aren't about what you report. They're about how your numbers match up with the forms the IRS already received. If your QuickBooks records don't reconcile with your 1099s, bank statements, and platform reports, you're setting yourself up for problems.

The good news? You can avoid all of this by getting your bookkeeping right before tax season hits. Here are five steps to make sure your QuickBooks Online records are clean, accurate, and ready to file without drama.

Step 1: Build Your Tax Folder Now (Not in March)

Start collecting documents the moment they arrive. Don't wait until your tax appointment to start digging through emails and bank statements.

Here's what you need to track down:

W-2s and 1099s (all types: NEC, K, MISC)

Mortgage interest statements

Brokerage and investment reports

Platform summaries (Stripe, PayPal, Square, etc.)

Payroll reports if you have employees

Receipts for major business expenses

If you're a service-based business owner, this step saves you from the nightmare of reconstructing your income later. Missing a 1099 or forgetting about a platform report means your reported income won't match what the IRS expects: and that's when notices start showing up.

Monthly bookkeeping makes this easier. When you're reconciling your accounts every month, you're already tracking income as it arrives. You're not scrambling in April to figure out where that $8,000 deposit came from.

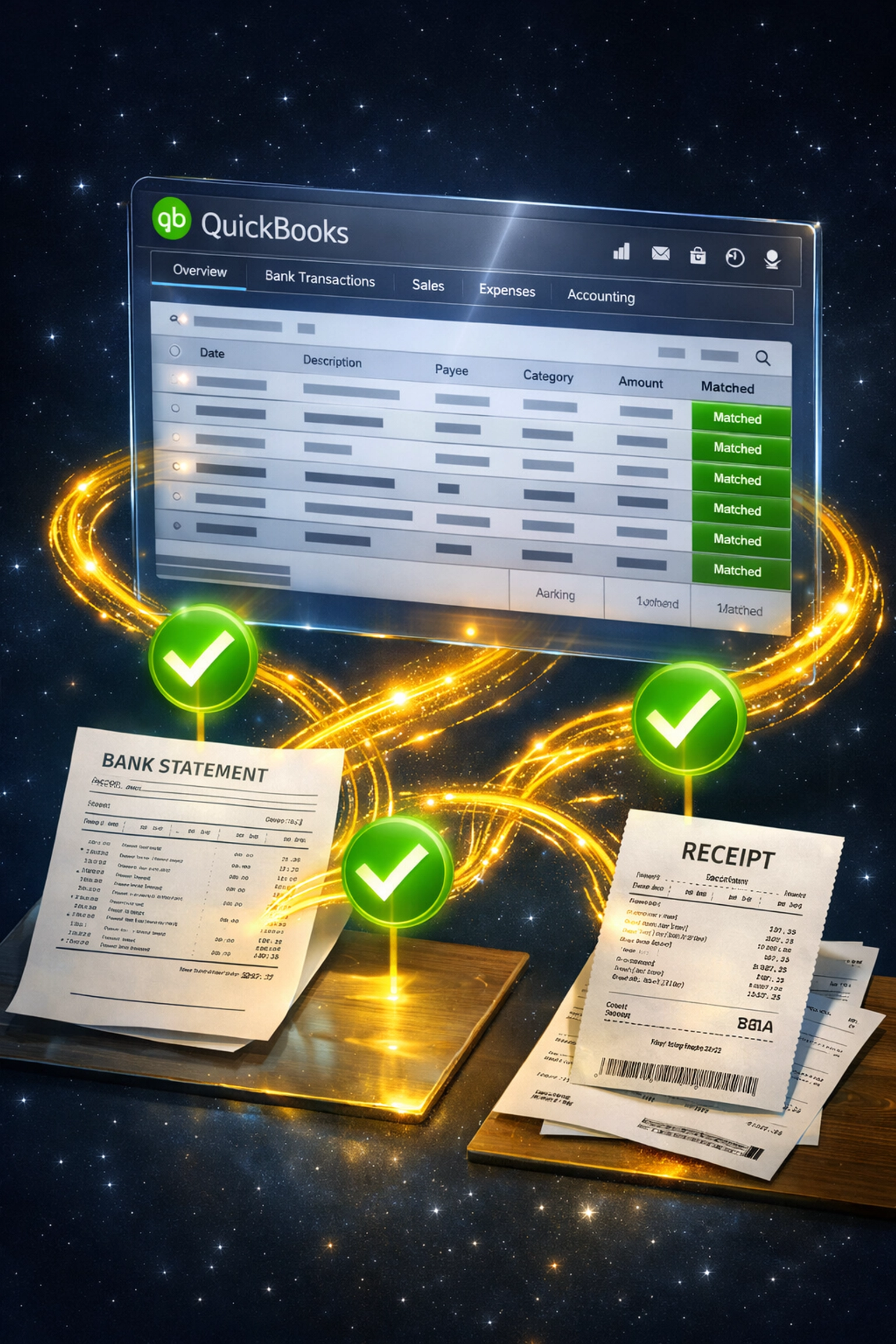

Step 2: Reconcile Every Account Before You File

This is non-negotiable. If your QuickBooks accounts aren't reconciled, your tax return is built on shaky ground.

Reconciling means matching your QuickBooks records to your actual bank statements and platform reports. Every deposit should tie back to an invoice or income source. Every expense should match a transaction in your business account.

Here's what happens when you skip reconciliation:

Your reported income doesn't match the 1099s the IRS received

Duplicate transactions inflate your expenses

Missing deposits make your profit look lower than it actually is

Uncleared checks throw off your cash balance

The IRS compares your tax return against third-party reports. If you report $75,000 in revenue but your platform issued a 1099-K for $82,000, you've got a problem. Even if the difference is legitimate, you have to explain it. And explaining mismatched numbers to the IRS is not how you want to spend your summer.

This is why monthly reconciliation matters. When you're staying on top of your books throughout the year, discrepancies get caught early. You're not trying to fix 12 months of errors in February.

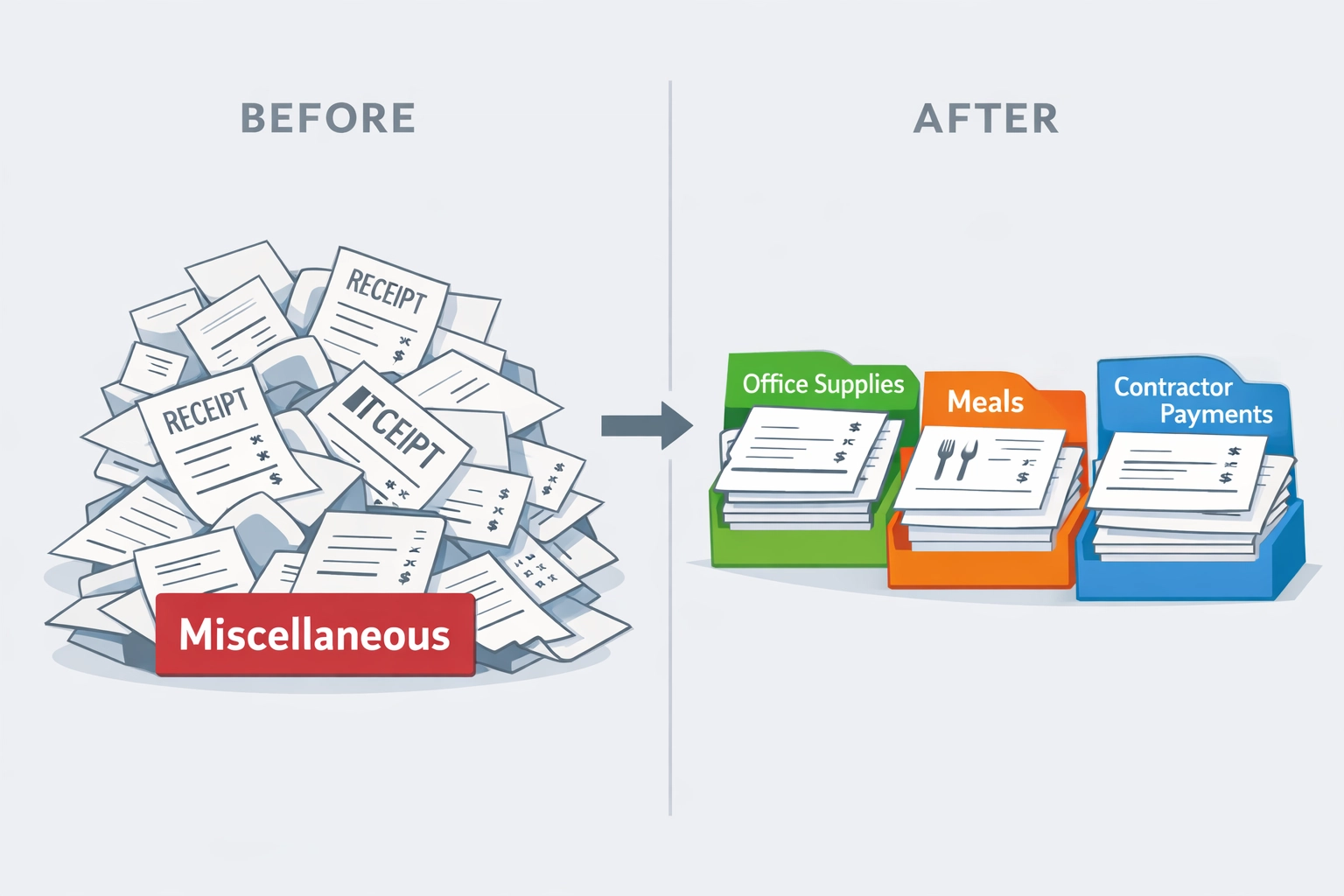

Step 3: Clean Up Your Chart of Accounts (No More "Miscellaneous" Buckets)

If your QuickBooks file has a giant "Miscellaneous Expense" category, your tax return is basically guesswork.

Here's the truth: proper categorization directly impacts your tax bill. When expenses are correctly classified, your CPA can maximize deductions and ensure you're compliant. When everything gets dumped into a catch-all category, you're either missing deductions or risking audit triggers.

Take a hard look at your chart of accounts:

Are business meals separated from office supplies?

Are contractor payments properly categorized as 1099 expenses?

Are personal expenses accidentally mixed into business accounts?

Are home office deductions properly tracked?

Cleaning up your categories isn't just about organization. It's about making sure your deductions hold up if you're ever audited. The IRS wants to see clear, defensible expense classifications: not a massive "Other" bucket.

A professional bookkeeper knows how to structure your chart of accounts. With monthly bookkeeping services starting at $297-$497 per month, you get expert categorization throughout the year. That means tax prep is faster, more accurate, and less stressful.

Step 4: Don't DIY QuickBooks Fixes (Especially for Closed Tax Years)

This one's critical: do not attempt to "fix" QuickBooks errors yourself, especially if those errors involve tax years you've already filed for.

Here's why. When you file a tax return, you're essentially locking in the numbers for that year. If you go back and change transactions in QuickBooks for 2024 after you've already filed your 2024 return, your books no longer match your filed tax return. If the IRS audits you, the discrepancies create major problems.

This is called the "Closed Period Trap," and it's one of the biggest mistakes small business owners make.

If you need to correct errors from previous years, a professional bookkeeper uses retained earnings adjustments to fix your current books without altering closed periods. This keeps everything clean, compliant, and audit-ready.

The DIY approach might seem cheaper upfront, but amateur accounting mistakes can trigger IRS algorithms in 2026. State and federal systems are better than ever at spotting inconsistencies. It's not worth the risk.

This is part of the Bookkeeping-First Tax Model. When your books are professionally maintained all year, you avoid the cleanup scramble before filing. Your numbers are accurate, reconciled, and ready to go.

Step 5: Wait for All Forms Before You File

Here's a trap that catches a lot of eager filers: you get your W-2 in January, plug your numbers into TurboTax, and hit submit. You feel accomplished.

Then in March, a corrected 1099 arrives. Or a K-1 from a partnership you forgot about. Or a brokerage form that didn't make the early deadline.

Now you're filing an amended return. And amended returns take longer to process, create more IRS scrutiny, and delay any refund you might be owed.

Don't file early. Some custodians and platforms don't issue 1099s until mid-February. Corrected forms can arrive even later. If you file before you have everything, you're guaranteeing yourself extra work and potential delays.

If you own an S corporation or partnership, file your business return first. Your K-1 flows through to your personal return, so you can't complete your 1040 without it.

Patience here pays off. Waiting until you have all your forms means filing once, filing correctly, and avoiding IRS notices later.

Your Tax-Ready Checklist

Before you file your 2026 return, make sure you can check these boxes:

✅ All tax documents collected (W-2s, 1099s, K-1s, platform reports) ✅ QuickBooks accounts fully reconciled through December 31 ✅ Reported income matches third-party forms ✅ Chart of accounts cleaned up (no giant "Miscellaneous" category) ✅ Documentation exists for all major deductions ✅ No DIY fixes made to closed tax years ✅ Business return filed before personal return (if applicable)

If you can't confidently check all these boxes, you're not ready to file yet.

The Bookkeeping-First Approach Prevents IRS Headaches

Here's the reality: most IRS delays aren't caused by what you report. They're caused by mismatches between what you report and what the IRS already knows.

The Bookkeeping-First Tax Model solves this problem by building your tax return on a foundation of clean, reconciled books. When your QuickBooks records are maintained monthly: not just fixed in February: your tax prep becomes faster, cheaper, and far less stressful.

You're not scrambling to explain discrepancies. You're not filing amendments. You're not getting surprise notices in June.

You're filing once, with confidence, and moving on with your business.

Ready to Clean Up Your Books Before Tax Season?

If your QuickBooks records are a mess, or if you're not sure your numbers will match what the IRS expects, let's talk.

Monthly bookkeeping services for service-based businesses start at $297-$497 per month. That includes professional software, expert categorization, regular reconciliation, and CPA-ready reports. You get clean books year-round: not just a pre-tax scramble.

Schedule a free consultation and let's make sure your 2026 filing goes smoothly.

Your books should support your business, not stress you out. Let's get them right.

Comments